Spill over effect: Using GARCH (1,1) model on eviews

Spillover Effect Analysis on Eviews | Finance Research Techniques | Bin Khalil AcademyПодробнее

Video 10 Estimating and interpreting a GARCH (1,1) model on EviewsПодробнее

GARCH Modelling for Volatility in EviewsПодробнее

Video 13 Estimating and interpreting GJR-GARCH (1,1) model on EviewsПодробнее

(EViews10): How to Estimate Standard GARCH Models #garch #arch #volatility #clustering #archlmПодробнее

GARCH model - EviewsПодробнее

CGARCH model - EviewsПодробнее

How to model and forecast volatility of series in Eviews:case of finanial seriesПодробнее

ATAL FDP - Research in Finance Using Eviews - Modeling Volatility using GARCHПодробнее

Video 14 Estimating and interpreting an EGARCH (1,1) model on EviewsПодробнее

EViews: (3 of 3) How to Estimate ARCH, GARCH, EGARCH & GJR-GARCH(or TGARCH) ModelsПодробнее

(EViews10):Estimate Fixed and Random Effects Models #fixedeffects #randomeffects #hausmantestПодробнее

Exploring the Returns and Volatility Spillover Effect in Taiwan and Japan Stock Markets AEFR 72 175Подробнее

RFM 2020 Lecture 5(4) Eviews Tutorial for Lecture 5 (GARCH-in-mean models)Подробнее

(EViews10) - How to Forecast ARCH Volatility #arch #forecasting #volatility #econometrics #modelingПодробнее

(EViews10) - How to Test for ARCH Effects #archeffects #archmodeling #volatility #heteroscedasticityПодробнее

How to estimate arch model - eviews tutorial completeПодробнее

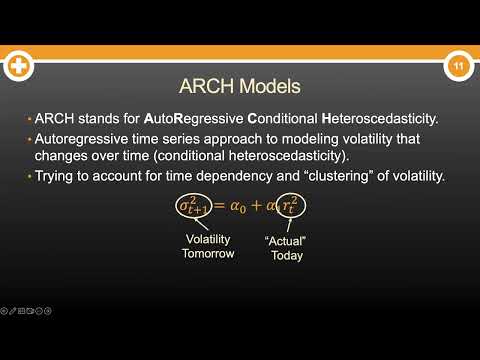

What are ARCH & GARCH ModelsПодробнее